One of the questions we get most frequently from our customers is how to save for retirement or how much they need to have saved by the time they reach a particular age.

Whether retirement seems like a long way off or just around the corner, it’s never too soon to set money aside for an emergency, to buy a home, or to start saving for retirement.

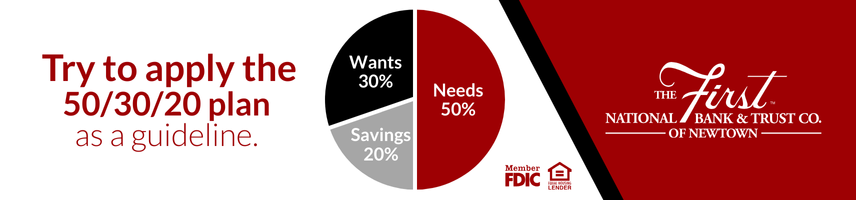

One general rule of thumb is called the 50/30/20 plan for allocating your take-home pay. The idea is that 50% of your take-home pay should be used for meeting your physical needs and necessities; 20% should be used for savings and paying off debts; and 30% should be used for things you want.

We can break this down into more detail like this:

• Needs (50%): Housing, food, transportation, utilities, insurance, and minimum loan payments.

• Savings (20%): Retirement plans, such as 401(k)s and IRAs, paying off debts, and establishing an emergency fund.

• Wants (30%): Subscriptions (streaming services and gym memberships), dining out, travel, entertainment, and nonessential clothes or home items (such as designer goods).

Regardless of age, other financial goals should involve building a credit score, or keeping your score as high as possible, and establishing an emergency fund. The size of your emergency fund depends on your needs. Financial experts recommend having an emergency fund of at least three to six months worth of your living expenses.

How Much Should I Have Saved in My 20s?

Most people in their early 20s are just getting started in life. Whether they’re graduating from college or entering the full-time workforce out of high school, things like home ownership and retirement can seem like they’re a million miles away.

One rule of thumb for a 21-year-old is to have $6,000 in a savings account for emergencies and long-term financial goals. Of course, this can be difficult when you’re most likely working at entry-level positions and may have student loans or other debts to pay off.

You may have to tweak the 50/30/20 plan to spend more of your income meeting your basic needs and adjust your budget to best fit your lifestyle.

Take a close look at your budget and spending habits each month to see if there’s any room to reduce your spending and set more money aside. If you have any kind of bonus funds, such as a raise or bonus from your employer, a scratch-off lottery ticket, or a birthday check from your grandma, try using these additional funds wisely by reducing debt or increasing your savings.

If your employer offers a 401(k) plan, aim to maximize your investment as much as possible. This is money you can have invested on a pre-tax basis, meaning you won’t have to pay any federal income taxes on these funds until you retire. If your company matches your contributions, you should make the most of this.

For example, if your employer offered a dollar-for-dollar match of up to 4% for all 401(k) contributions, and you put 4% of your income into your 401(k) you’d be getting an additional 4% of your salary added to your retirement fund for free.

By starting early with your retirement savings, you can take advantage of compound interest and watch these funds grow dramatically over time.

How Much Should I Have Saved by Age 30?

By age 30, financial experts say you should have at least one year’s worth of your income in savings. If you make $55,000 per year, then you should try to have that much saved.

Of course, you might have other concerns such as starting a family or saving up to buy a home. Maybe that old car you inherited from your grandparents is nearing the end of its lifespan.

Here are some ideas that can help you get on track with your budget and savings:

Prioritize Your Emergency Fund

While you might seem to have more pressing needs, especially if you’re starting a family, growing your emergency fund can help you protect your other assets.

If something comes up, such as an expensive car repair, you’re probably better off tapping into your emergency fund instead of paying it off over time on your credit card, with high-interest payments.

Using your emergency fund is also better than tapping into your retirement funds, such as your 401(k), as you would have to pay a financial penalty for early withdrawals. You would also lose out on the growth potential of your retirement account.

Focus on Your Highest Interest Debts

While making the most of your 401(k) account and building an emergency fund should remain top priorities, if you have any debts then it’ll be important to pay them off as quickly as possible.

Take a close look at where you stand on each one and what the interest payments are. If your student loan debt is at a relatively low interest rate, and you’re paying a high amount of interest on one or more credit cards you might focus on paying off those cards as quickly as possible. Removing this debt burden can save you a considerable amount of money in interest payments.

Automate Your Savings

If you use direct deposit for your paychecks, consider having a portion of each paycheck transferred into a personal savings account as your short-term emergency fund. You can also use this fund to save up for a down payment to buy a home.

Having a certain amount automatically set aside and resisting the urge to tap into your emergency fund can help you reach your financial goals and serve as financial insulation against unforeseen contingencies.

Consider High Yield Savings Accounts and Certificates of Deposit (CDs)

While regular savings accounts do earn interest, you have other options of where to keep your money. As your emergency fund grows, you might put some of it into a high-yield savings account or certificates of deposit.

Money market accounts have higher deposit requirements than standard savings accounts, but they also offer higher interest payments based on how much you hold in your account. They also let you access your funds whenever you need them.

Certificates of deposit are available at maturities ranging from three months to five years. Many people keep some of their emergency funds in a savings or money market account, which they can readily access. They also keep some of their funds in CDs with different maturity dates. This allows them to maximize their interest earnings while seeing that some of these funds would be accessible at given points throughout the year.

Put Your Retirement Goals Ahead of Your Kids Education

While saving up for college tuition, and any other education costs, are at the top of mind for many parents, if you have to choose between your own retirement fund and a college fund, many experts recommend their retirement should come first.

By focusing on your retirement, you can watch your retirement fund grow over time with compound interest. The more you have for retirement, the less likely you’ll be a financial burden on your kids later on.

Your kids, on the other hand, have options for funding their education. They could be eligible for financial aid such as scholarships, grants, and student loans. They might choose a school that’s more affordable rather than the school of their dreams.

Simply put, your options for saving for retirement are more limited than your kid’s options for how they’ll pay for school. After reaching a point where you know you’ll have enough for retirement, then you could focus on a college fund.

Work with a Financial Advisor

Every person’s financial situation and needs are different from those of their peers. A financial advisor can take a close look at where you stand and help you meet your financial goals.

How Much Should I Have Saved by Age 40?

By age 40, financial experts recommend having three times your annual salary in savings and three to four times your annual income by age 45. Another rule of thumb is to set aside $1,000 or more each month, in savings and retirement funds.

If you haven’t saved very much for your retirement, or not at all, it’s important to get started on this as soon as possible. Take a close look at your retirement funds and how to set aside as much as possible. Remember that the more you set aside now, the more you’ll make in compound interest as your investment grows over time.

Working with a financial planner could help you figure out what kind of lifestyle you’d like to live in retirement, what kind of contingencies could happen, how much you’ll need for your golden years, and how to draft a plan to meet your retirement goals.

Focus on Your Retirement Funds

If your employer doesn’t offer a 401(k) plan or a 401(k) match, you might consider looking at your employment options and whether you could earn more money, both in terms of your income and retirement fund.

In addition to a 401(k), you might consider a Roth IRA and a health savings account (HSA) if your employer offers one.

Use a Health Savings Account (If Available)

Health savings accounts let you set money aside on a pre-tax basis that you can spend on medical care, such as doctor visits and prescriptions. One of the great benefits of HSAs is whatever money you set aside is yours forever, similar to a 401(k) fund.

With many HSA funds, you can have this money invested just like you do with your 401(k). Another benefit is you won’t have to pay any taxes on your HSA funds, as long as you spend this money on medical needs.

In a way, HSAs are like a retirement fund for your healthcare needs—and your medical bills are likely to get more expensive as you age.

The maximum HSA contribution limits for 2025 are $4,300 for individuals and $8,550 for families. Those age 55 and older can make an additional catch-up contribution of $1,000.

How Much Should I Have Saved by Age 50?

By age 50, financial advisors recommend having six times your annual income in savings. If you feel like you’re not saving enough for retirement, you might try to maximize your 401(k) and IRA contributions.

The total 401(k) contribution limit for 2025 will be $23,500 for employee contributions and $70,000 for combined employer and employee contributions. Those aged 50 to 59 can make an additional “catch-up contribution” of $7,500. Those between 60 and 63 can make catch-up contributions of $11,250.

Contribution limits for Roth 401(k) plans are the same as those for traditional 401(k) plans. A qualified financial advisor can help you decide how much you need to contribute and whether an IRA would make sense.

How Much Should Have Saved by Age 60?

Another way to put this is “How much should I have saved for retirement?” By age 60, financial experts recommend that individuals have saved up to eight times their annual income, although some would say you might need more than that based on your salary, health needs, and lifestyle.

If that age is decades away for you, try considering what your annual income could be at that age and how much you’ll need to save before you reach that point.

You can also use the Social Security Administration’s Social Security Estimator to get an idea of what your Social Security benefits would be at three different stages of your life:

• Age 62 is the earliest age at which you can claim Social Security benefits, but retiring early would permanently reduce the benefits you would receive for the rest of your life.

• Age 66 to 67, also known as your full retirement age (FRA). Retiring then would entitle you to 100% of your Social Security benefits.

• Age 70. The later you retire past your FRA, the more you could receive in Social Security payments. This maxes out at age 70, at which point you’d receive 124% of what you would’ve received at age 67.

Start Saving at Any Age with First National Bank and Trust

Whether you’ve been saving for years or just realized you need to start saving for retirement, we can help you with financial planning at every stage of life. Please contact us to speak with a wealth manager or CERTIFIED FINANCIAL PLANNER® professional. We can help you open a savings account or a retirement account, and help you find the right path to financial security. You can also visit one of our convenient locations.